The Strait of Hormuz, the narrow channel through which around a fifth of the world's oil flows, was closed for eleven weeks at the start of the year and despite marginal re-opening under an Iran-administered toll regime, remains effectively closed.

In this environment, Britain's conservatives from centrist to extremist, have rediscovered an old enthusiasm. Reopen the North Sea, the Telegraph demands. Drill, baby, drill, says GB News. Reform UK has placed the reversal of Ed Miliband's Energy Independence Bill — the legislation that proposes to ban new oil and gas exploration licences in British waters for new fields — at the top of its manifesto. The Tories have launched a "Get Britain Drilling" Bill.

The argument seems intuitive enough. Prices are high and imports are exposed. Britain has hydrocarbons beneath its own waters that are going unused. Why not?

We decided to look into it a bit more deeply. One of us is a complex systems theorist specialising in the intersection between energy and society. The other is a former industry veteran who headed up Shell Asia's low carbon fuels division. We decided to model what would actually happen if Britain did exactly what Reform UK, the Conservative Party and the fossil fuel industry keep demanding.

Here's our methodology for anyone that wants to test the model out themselves.

And here's the clean Python code:

Our findings are astonishing: drilling in new fields in the North Sea would not only be pointless from an energy sovereignty point of view; it would cost the British state hundreds of millions in net losses. The only ones to benefit?.... a few oil and gas companies.

Executive Summary

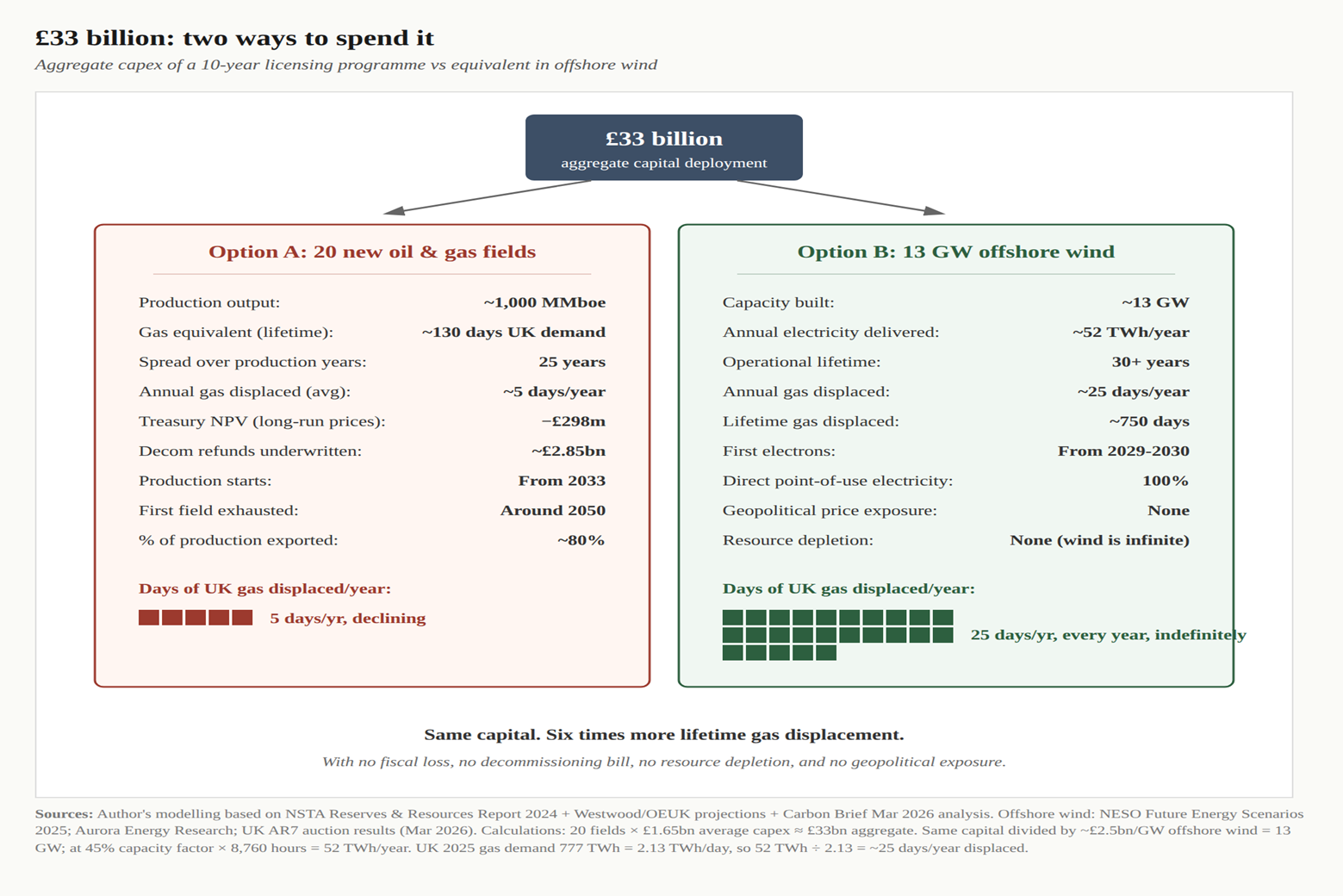

What a ten-year reopened licensing programme would deliver

A reopening of the kind Reform UK proposes would issue around 50 new licences per year for a decade, or 500 in total. At the empirical conversion rate from the previous Conservative years, around 20 of those licences would become producing fields. Construction would begin in the late 2020s, with first oil and gas arriving from 2033 onwards. Across the production lives of all 20 fields combined — roughly 25 years of operation — the cumulative output would equal about 130 days of UK gas demand, or approximately five days of gas per year on average, declining over time as the fields aged.

Roughly 80% of the oil component would be exported to refineries elsewhere; the gas would feed into a UK market that prices the molecule at the international rate regardless of its origin.

What it would cost the British state

Building those 20 fields would require approximately £33 billion of capital investment. Across the full lifetime of the programme, modelled at long-run forward-curve gas and oil prices, the British Treasury would lose approximately £298 million in net present value (NPV) — meaning that when the tax receipts over the field lives are tallied up in today’s money, after deducting the refunds the state must pay back to operators at the decommissioning stage, the total comes out below zero.

In addition, the state would contractually underwrite around £2.85 billion of decommissioning refunds — the British public’s share of dismantling the platforms, drawn from HMRC’s estimate that taxpayers cover 29% of the industry’s decommissioning bill.

The £298 million Treasury loss is a modelled figure, but its direction and magnitude line up with independent analysis of comparable fields.

How this measures against the cost of staying gas-dependent

The Office for Budget Responsibility's 2023 Fiscal Risks and Sustainability Report calculated that continued UK gas dependency, under recurring decade-scale price shocks of the kind seen in 2022 and now again in 2026, would add approximately 13% of GDP to British public debt by 2050.

In today's money this is £364 billion. The total public cost of the licensing programme — £298 million in modelled Treasury loss plus £2.85 billion in contractually committed decommissioning refunds — is approximately £3.15 billion. Set against the OBR’s £364 billion gas-dependency fiscal exposure, this is a ratio of roughly 115 to one: for every pound of public money the state commits to new licensing, continued gas dependence costs the Treasury £115 in absorbed price shocks.

Every new field added to the British system locks in another 22 years of commitment to the very global gas market that is the source of this fiscal exposure.

What the same money would buy in renewables

The £33 billion of capital required for the licensing programme, if deployed instead in offshore wind at current development costs of approximately £2.5 billion per gigawatt, would build approximately 13 gigawatts of new offshore wind capacity. Over a 30-year operating life, that capacity would displace about 25 days of UK gas demand every year, indefinitely — five times more than the licensing programme would deliver, and with no decommissioning bill at the end of life and no exposure to global supply shocks.

What the previous Conservative experiment already showed

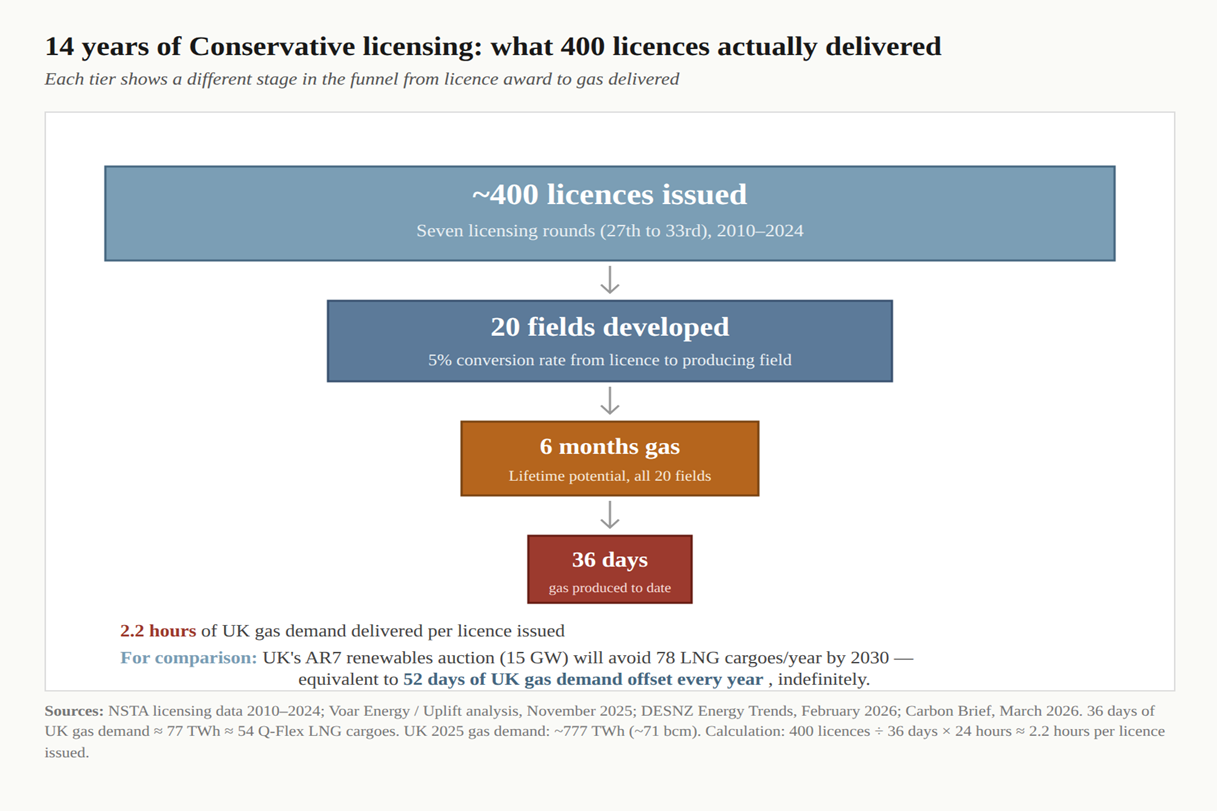

Britain has already run this experiment, by the way. Between 2010 and 2024, Conservative governments issued approximately 400 new offshore licences across seven licensing rounds. Of those, only twenty fields were actually built.

Their combined production so far amounts to a whopping.... 36 days of UK gas demand; their combined remaining potential, when fully exhausted, is around six months.

Divide cumulative production by licences issued and the answer is two hours and twelve minutes of UK gas demand per licence.

The most recent renewables auction will displace more than that in every twelve hours of operation, indefinitely.

The verdict

The case for reopening licensing fails on its own chosen criteria. Oil and gas from a 2026 licence cannot arrive before 2033 at the earliest due to development time-spans, so new licences are literally useless for near-term supply.

The tax system, through capital expenditure relief, ten-year compounded loss uplifts, and decommissioning refunds, neutralises the headline 78% tax rate, so the Treasury gains nothing in net revenue.

Britain pays the international gas price regardless of where the molecule is extracted, so bills stay where the global market sets them. And every new field is a 22-year political and infrastructural commitment to the very dependency costing Britain £364 billion across the OBR’s projection horizon — actively deepening the fiscal exposure that reopening is supposed to reduce.

Strip the political rhetoric away and what remains is a transfer of public money to private operators in exchange for a quantity of energy that is, in the context of national demand, statistically marginal.

To understand how we reach these figures, read on.

What 14 years of licensing actually delivered

The figures from the Conservative years come from a November 2025 analysis by Voar Energy and the campaign group Uplift, drawing on North Sea Transition Authority data. They are uncontested by industry.

Between 2010 and 2024, Conservative governments issued approximately 400 new offshore licences across seven rounds. Each licence grants an operator the right to explore a specified block of seabed and, if the geology proves promising, to apply to build a production facility. Of the 400 awarded, just 20 were turned into producing fields; the remaining 380 sat unused in company portfolios, were eventually surrendered to the regulator, or never crossed the threshold of economic viability. The conversion rate from licence award to producing field works out at 5%.

Those 20 fields have so far delivered 36 days of UK gas demand between them. Their combined remaining potential, fully exhausted, is around six months. The lifetime total per licence ever to be issued is therefore approximately 13 hours of UK gas, with 2.2 hours of that produced to date.

The most recent UK renewables auction, known as AR7, gives the relevant comparison. The auction is the seventh round of a programme that pays wind and solar developers a guaranteed price per unit of electricity for fifteen years; this year's round locked in roughly 15 gigawatts of new wind and solar capacity. By 2030, when those plants are operating, they will displace gas demand that would otherwise have to be met by imports, at a rate of around 52 days of UK demand per year, every year, for their working lives.

One year of renewables procurement delivers, in a single year of operation, considerably more gas displacement than fourteen years of fossil licensing produced across their entire lifetimes.

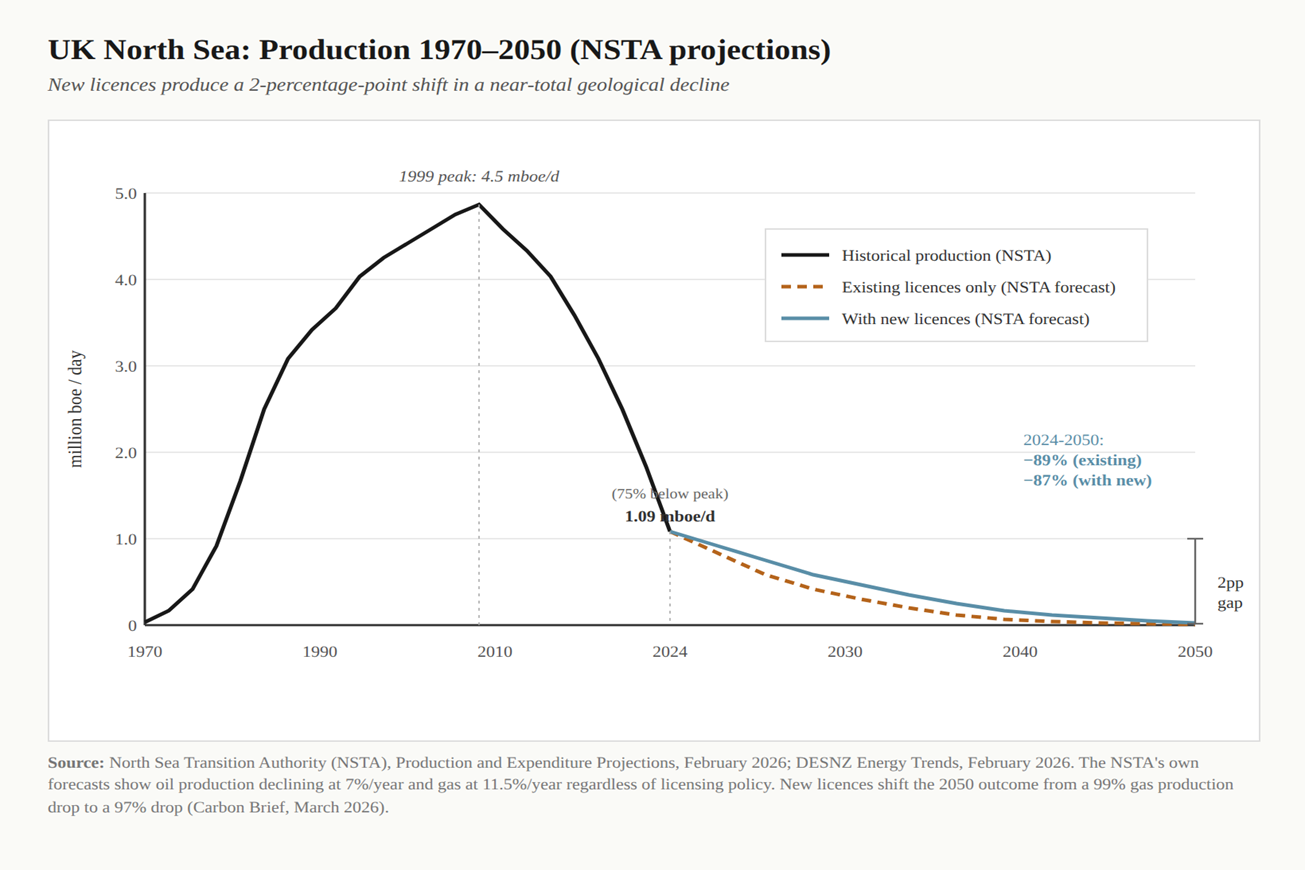

The geology explains the disappointing yield. UK Continental Shelf (UKCS) production peaked in 1999 at 4.5 million barrels of oil equivalent per day. By 2024 it was 1.09 million, a fall of 75%. The North Sea Transition Authority forecasts further declines of 7% per year for oil and 11-12% per year for gas through 2030. Even on the most optimistic licensing scenarios, total UKCS output drops a further 87% by 2050. The basin is what the regulator itself calls "ultra-mature." It is, by any reasonable definition, geologically exhausted.

New licences cannot help the current crisis

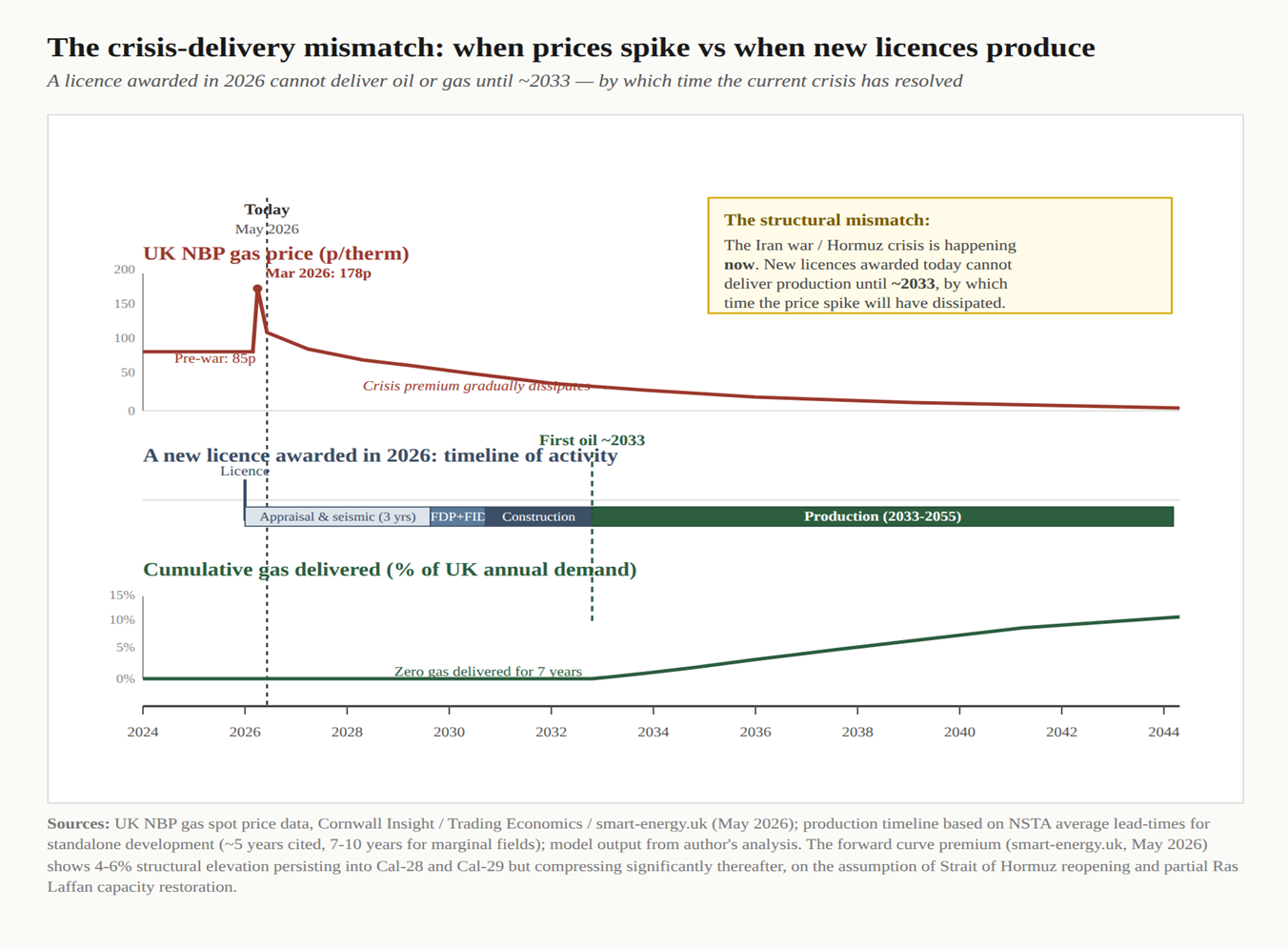

The seven-to-nine year gap between licence award and first production is the most fundamental problem with the case for reopening. Politicians and campaigners speak as though approval of an exploration block today translates somehow into lower energy bills next winter. BBC News pundits sit and listen to this garbage without offering challenge, as if it's sensible.

It's actually embarrassingly stupid.

The North Sea Transition Authority cites five years as the average time from licence award to first production. That figure refers to tiebacks — small discoveries that can be plumbed into the pipework of an existing nearby platform without building new infrastructure. Most of the genuinely new opportunities in the basin require standalone development. For those, the realistic timeline is seven to nine years and often longer. The Rosebank field, one of the largest North Sea developments in decades, was discovered in 2004 and first oil is expected in 2026-27. That is twenty-two years from discovery to production.

A licence awarded today therefore moves through appraisal in 2027-28, a Field Development Plan in 2029, a final commitment to build the field around 2030, construction in 2031-32, and first production in 2033 at the earliest. Neither Farage nor Badenoch talk about this. Strangely, the hapless pundits who interview them seem to have no idea either.

By the time the oil and gas arrive, the prices that justified the development will have shifted. Financial markets already price this in. The forward curve — what futures contracts for delivery in coming years are trading at — shows a 4-6% structural premium on UK gas for delivery in 2028 and 2029 relative to pre-war norms, then progressive normalisation as Ras Laffan rebuilds and supply chains adjust. By 2033 the crisis premium has substantially decayed. The capital markets confirm this. Major North Sea operators apply a minimum return-on-capital threshold of 15% before committing to standalone development; at long-run forward-curve gas prices, the median undeveloped UKCS discovery falls below that threshold before financing costs are even applied. The block lies in the underlying resource economics, not in regulation or tax. No amount of licensing activity changes that.

This produces an awkward position for any operator considering a 2026 licence. The capital cost is incurred in 2030-2032, at prices for steel, contractors and offshore services that the Iran war has elevated. The revenue arrives from 2033 onwards, into a market that has, likely by then, reverted toward pre-crisis pricing. Costs are paid at war-elevated rates; production is sold at post-crisis rates.

If the post-Hormuz environment justifies any kind of supply response involving North Sea oil and gas, the only response that can help in any meaningful timeframe is accelerated production from existing licences. That is already under way. On 1 December 2025, Equinor and Shell UK merged their British operations into a joint venture called Adura, explicitly aimed at extracting maximum value from their existing UKCS assets while prices remain elevated.

New licences are irrelevant to this dynamic because they cannot produce anything before the dynamic has passed. The Adura merger is also a capital-allocation signal that the industry itself rarely articulates plainly: when two of the largest operators in a basin consolidate rather than compete for new acreage, they are telling investors that organic growth from new drilling has ceased to be the value-creation strategy. Portfolio optimisation, cost reduction, and life extension on existing infrastructure is now the rational play.

Who actually pays, and who actually profits

How the British state taxes oil and gas explains why the Treasury loses money on most new fields while operators profit anyway.

Profits from oil and gas extracted from British waters are taxed under three overlapping regimes that together set what is called the "headline rate." There is Ring Fence Corporation Tax at 30%, an additional Supplementary Charge at 10%, and a temporary Energy Profits Levy at 38% that Chancellor Rachel Reeves extended in November 2024 until March 2030. Stack the three together and the total tax rate on North Sea profits is 78% during the Energy Profits Levy period, dropping to 40% from April 2030 onwards. The headline rate sounds punitive, and is meant to. In practice, four features built into the system gut its effect.

We set out four things - forgive us for some of the technical details, but they are important - which mean the British state will lose billions if it allows new North Sea licensing in new fields.

The first feature is the immediate tax write-off for capital expenditure. Under what is called the "capital allowance," 100% of money spent building a field can be deducted from taxable profits in the year the spending happens. A company spending £2 billion building a platform reduces its taxable profits by £2 billion that year. Since the company has not yet started producing oil during the seven-to-nine year development phase, there are no profits to reduce; the deductions are carried forward as "losses" to be used against future profits when they eventually arrive.

The second feature inflates those carried-forward losses year on year. Through a mechanism called the Ringfence Expenditure Supplement, unused losses grow by 10% per year, compounded, for up to a decade. A £2 billion loss pool, sitting unused for eight years and uplifted at 10% compound, becomes a £4.3 billion loss pool by the time meaningful production revenue arrives. The operator then deploys this larger pool against its profits, eliminating tax liability for several more years. Norway's state oil company Equinor used this single mechanism to extract £400 million in UK tax relief in 2021 and 2022 alone.

The third feature concerns timing. For a licence awarded in 2026, almost all the capital spending falls before April 2030, the end of the Energy Profits Levy period. Operators effectively bank tax relief at the higher 78% rate while paying tax at the lower 40% rate when revenue eventually arrives.

The fourth feature is decommissioning. When a field eventually exhausts, the operator must dismantle the platforms, plug the wells and remove the infrastructure. The North Sea Transition Authority estimates the total industry decommissioning bill at £41 billion. HMRC's own figures show that the British taxpayer covers £11.7 billion of that, or 29%, through tax repayments and forgone corporation tax. Through 109 Decommissioning Relief Deeds signed since 2013, the government has contractually committed to those repayments.

The consequence of these four features is that a typical new field can run for its entire 22-year life without paying any net tax, while still requiring the Treasury to issue refunds at the decommissioning stage. The operator collects the revenue. The British public collects the bill.

The contrast with comparable hydrocarbon regimes is glaring. Norway retains 67% state equity participation in new fields through Equinor (formerly Statoil); Qatar runs the world’s largest LNG programme through QatarEnergy as majority partner in every joint venture. In both, the state captures resource upside directly.

Unfortunately, in true neoliberal form, the UK chose the opposite model: private operators hold the equity, the state holds tax claims, and as this analysis shows, the tax claims are worth less than zero at realistic prices.

The asymmetry shows up clearly in what large operators actually pay. Equinor reported global pre-tax profits of approximately £141 billion across 2022, 2023, 2024 and 2025 combined — around £45,000 per second across the energy-crisis years. In 2022 alone, on roughly £1 billion of UK profit, Equinor paid £6 million in UK tax, and zero on its UK oil and gas operations. The system performs exactly as designed.

One further mechanism amplifies all four. When an operator sells a field — as Equinor sold Rosebank’s operatorship to Ithaca Energy — the accumulated tax loss pool transfers with the asset. The buyer inherits not just the geology but the full uplift-augmented shield against future tax liability. The subsidy is fully priced into the transaction: the seller captures it as a valuation premium, the buyer deploys it to wipe out tax on production revenue, and the British public funds the benefit twice over.

Run the numbers

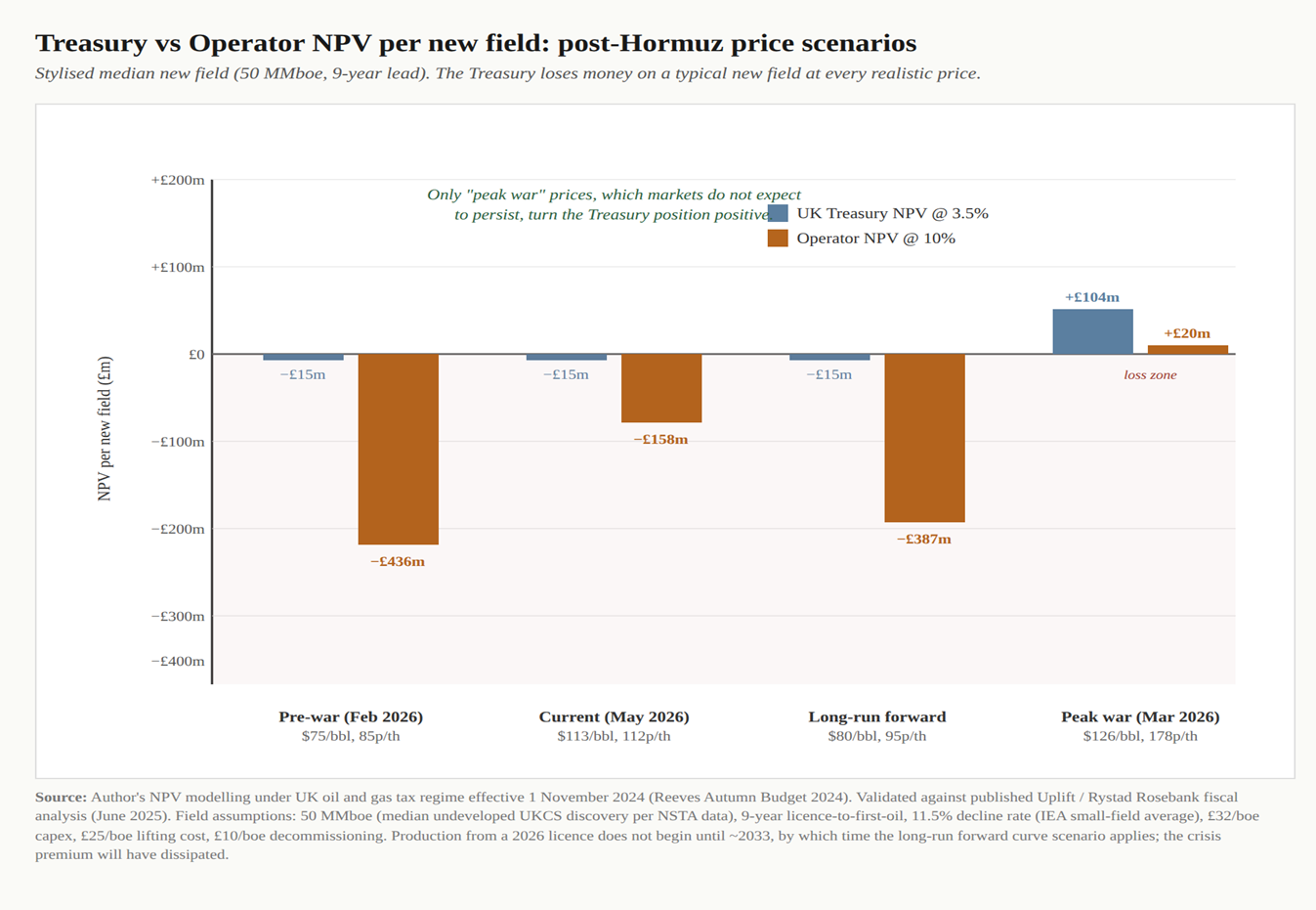

So let's test the licensing case against a representative new field across realistic price scenarios. The parameters below describe a median new development of the kind 2026 licences would actually be expected to produce, drawn from current official data.

The field contains 50 million barrels of oil equivalent — what the industry calls "MMboe," meaning the energy in 50 million barrels of oil when gas reserves are converted into oil-equivalent units. This is the middle of the range of undeveloped discoveries in the NSTA’s database. Seventy per cent of the field is oil, 30% gas. From licence award to first production: nine years. From first production to exhaustion: 22 years. Operating decline rate after the plateau: 11.5% per year, which the International Energy Agency gives as the average for small offshore fields globally. Cost per barrel to build (capital expenditure): £32. Cost per barrel to extract once built (operating cost): £25. Cost per barrel to dismantle at end of life: £10.

Run through a 30-year cash-flow model under post-November-2024 tax rules, the Treasury position (what the field adds to public finances after decommissioning refunds, in today’s money) and the operator position (what the company keeps after tax, at commercial discount rates) come out as follows.

|

Scenario |

Oil $/bbl |

Gas p/therm |

Treasury |

Operator |

|

Pre-war (Feb 2026) |

75 |

85 |

−£15m |

−£436m |

|

Current (May 2026) |

113 |

112 |

−£15m |

−£158m |

|

Long-run forward curve |

80 |

95 |

−£15m |

−£387m |

|

Peak war (Mar 2026) |

126 |

178 |

+£104m |

+£20m |

The pattern is clear. The Treasury loses money on the typical new field at pre-war prices, at current post-Hormuz prices, and at the long-run forward curve — the price environment the field actually sees when it begins producing in the mid-2030s. Only at peak war prices, which the futures markets themselves expect to fade, does the Treasury position turn modestly positive.

The operator’s position is similar: it loses money in three of four scenarios, which is precisely why most marginal North Sea discoveries never get developed. Why, then, do any operators develop North Sea fields at all?

Global portfolio logic. Majors such as Equinor and Shell book reserves across their worldwide operations; a UKCS discovery contributes to reserves replacement ratios significant to investor relations and credit ratings regardless of the UK-specific cashflow. The marginal field is carried by the global balance sheet rather than justified on its own numbers. The development decision is made in Oslo or The Hague, against a global benchmark that UK tax policy cannot meaningfully shift — which is precisely why state fiscal incentives are superfluous.

Scaled across a full 10-year licensing programme — 500 licences, 20 producing fields — the aggregate Treasury position at long-run forward-curve prices is a loss of £298 million in today’s money, plus the contractually underwritten £2.85 billion of decommissioning refunds the state pays out when the fields reach end of life. Aggregate capital required for the build-out: £33 billion. Aggregate gas produced over 25 years: 130 days of UK demand — about five days a year on average, declining over time. For five days a year of gas, of which 80% is exported, the British state underwrites a £33 billion capital programme and accepts a multi-billion-pound exposure to the operators’ end-of-life costs

What the same money would buy

The 20 fields of a decade-long licensing programme require roughly £33 billion of capital investment. Recent UK contracts-for-difference auctions for offshore wind, confirmed by BEIS project-level data, put the build cost at approximately £2.5 billion per gigawatt. At that rate, £33 billion buys approximately 13 gigawatts of new offshore wind capacity. With a capacity factor of 45% (the share of time the turbines run at full output), 13 gigawatts produces around 52 terawatt-hours of electricity every year, for a 30-year operating life.

In gas-displacement terms, the fossil licensing programme replaces around five days of UK gas demand per year on average. Yes it's "sovereign energy". But it's unquestionably negligible. It is not worth the return on investment.

The renewables programme replaces around 25 days per year, every year, indefinitely — 130 days of gas-equivalent from the oil and gas fields over their full lives, against 750 days from the offshore wind. Roughly six times the lifetime energy, delivered as electricity straight to British homes and businesses rather than as oil exported for refining (which is largely what happens to North Sea oil and gas anyway rather than being used domestically). And this is purely capital-for-capital, before the fiscal arithmetic, or the seven-year delivery mismatch enters the picture.

The £364 billion question the government has already answered

The most decisive argument comes from the Office for Budget Responsibility itself — the British state’s official independent forecaster, whose remit is to assess the credibility and risks of government fiscal policy.

In its 2023 Fiscal Risks and Sustainability Report, the OBR modelled what would happen if Britain maintained its current level of dependence on global gas markets while those markets continued to deliver decade-scale price shocks of the kind seen in 2022, and now again in 2026. Each such shock costs the British Exchequer between 2 and 3% of GDP in fiscal support for households and businesses — energy price guarantees, business support schemes, debt interest on the additional borrowing. Repeated every decade through 2050, these shocks would add approximately 13% of GDP to public debt. In today’s money, that is around £364 billion.

In the OBR’s own words, the cumulative cost of gas dependence comes out at "about twice as much as the 6% of GDP central estimate for the total cost of public investment to complete the transition to net zero by the middle of the century."

Set this £364 billion exposure against the total public cost of a decade of reopened licensing — £298 million in modelled Treasury loss plus £2.85 billion in contractually committed decommissioning refunds, roughly £3.15 billion in total.

The ratio is 115 to one: for every pound of public money committed to new licensing, continued gas dependence costs the Treasury £115 in absorbed price shocks. Since the licensing programme costs the state money in every realistic price scenario, there is no positive offset to chip away at the £364 billion.

So this is not a choice between two rival fiscal strategies. The licensing programme actively deepens the gas-dependence exposure rather than reducing it, because every new field locks in another 22 years of British infrastructure and political commitment to a global market that is itself the source of the fiscal vulnerability. The cure prescribed by the right-wing politicians and pundits makes the disease worse.

A better response

A serious response has four components. First, Britain should accelerate the build-out of offshore wind, solar and electricity grid infrastructure to displace gas demand permanently. Second, the Warm Homes Plan, currently £15 billion in scale, should expand: insulating British homes and electrifying heat reduces gas demand at source, where it does most fiscal and household good. Third, existing North Sea licence holdings should be allowed to maximise short-term output where this can usefully contribute to market balance — exactly what the Adura joint venture and similar arrangements are already doing under the current policy framework. Fourth, and underweighted in the current policy debate, the UK needs proper transition finance architecture: a recapitalised Green Investment Bank model could mobilise four to six pounds of private capital into offshore wind and grid infrastructure for every pound of public commitment, multiplying the same fiscal headroom that the licensing programme would dissipate on decommissioning guarantees.

New licensing has no place on this list. The barrels arrive too late, the costs structurally favour the operator over the public, the energy return sits below the threshold at which extraction is rational, and the opportunity cost of the capital runs to multiples of what the same money would deliver in renewables. On every measurable calculation, the licensing programme deepens the very fiscal exposure it claims to reduce.

The North Sea has paid its dues. Its revenues helped modernise Britain in the 1980s and 1990s. Geologically and fiscally, the basin is now in its declining phase, and no amount of political enthusiasm changes the underlying mathematics.

The campaign now under way to reverse UK Energy Secretary Ed Miliband’s licensing ban amounts to fiscal vandalism dressed as patriotism — but its costs would fall directly on the working-class households whose energy bills the campaigners claim to be defending. The benefits would accrue, instead, to Equinor, Shell, Ithaca Energy and their peers, who have collected them through every previous cycle and stand ready to collect them again.