A Strategic Foresight Report for Investors in an Emerging Climate Risk Regime – AoT Planetary Intelligence Bulletin

Executive Summary

Key Insight

New evidence suggests that two of Earth’s planetary climate regulators—the Atlantic Meridional Overturning Circulation (AMOC) and Southern Ocean overturning circulation—may be approaching irreversible tipping points before 2050. Their collapse would trigger nonlinear macro-financial shocks with systemic implications for global markets, sovereign credit, and institutional portfolios.

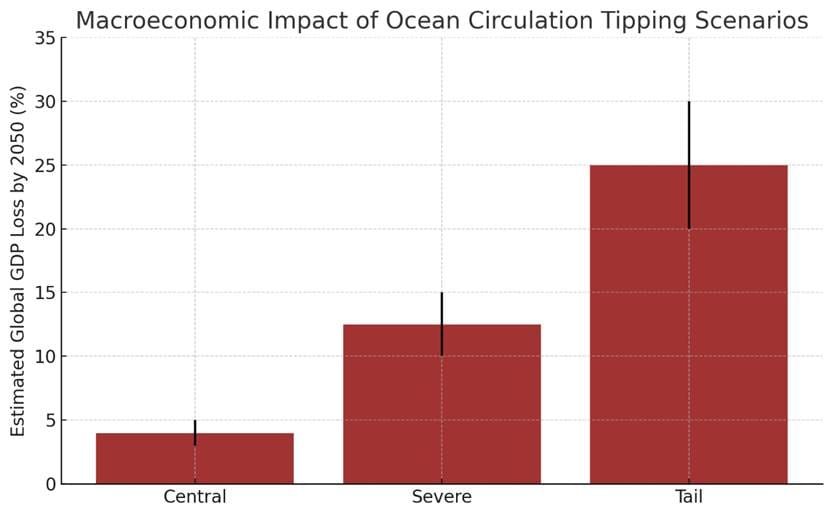

3 Risk Scenarios to 2050

|

Scenario |

Temperature |

System

Status |

GDP

Loss |

Credit

Risk |

|

Central |

~2.0 °C |

Moderate slowdown |

3–5% loss |

Mild CDS widening |

|

Severe |

~2.5–3.0 °C |

Significant weakening |

10–15% loss |

Sovereign downgrades |

|

Tail |

3.0 °C+ |

Collapse of AMOC + Southern

Ocean |

20–30%+ loss |

CDS >1000bps; defaults

likely |

Top 3 Financial Implications

- Sovereign Credit Disruption

– Climate-tied rating downgrades, bond volatility, and regional debt crises - Asset-Class Repricing

– Breakdown in diversification logic; equities, insurance, and real assets face systemic devaluation - Infrastructure and Food System Collapse Risk

– Tipping cascades may trigger compound failures across agriculture, insurance, and public systems

Key Early-Warning Signals to Watch

|

Indicator |

Threshold |

Action |

|

AMOC slowdown (RAPID) |

>20% vs baseline |

Reduce EU exposure |

|

Salinity rise (Southern Ocean) |

+0.5 PSU |

Hedge carbon & commodities |

|

CDS spreads (EM sovereigns) |

>500bps |

Exit/rotate to green sovereigns |

Strategic Allocation Implications

|

Asset

Class |

Tail

Scenario Exposure |

Resilience

Strategy |

|

Equities |

–35% loss |

Shift to climate-aligned

sectors |

|

Sovereign Bonds |

–25% loss |

Exit high-risk EM, add green

bonds |

|

Real Assets |

–40% in coastal RE |

Reallocate to high-latitude

farmland |

|

Insurance |

–50% loss |

Limit exposure; use CAT bonds |

|

Liquidity |

Preserved |

Increase allocation, maintain

optionality |

Conclusion

This is not a distant risk. Nor is it any longer meaningful to relegate these scenarios to a low-probability event given the new signals of dangerous feedback loops emerging. It is a civilizational inflection point unfolding within strategic investment horizons. Institutional portfolios must be redesigned to navigate an emerging climate regime defined not by linear change, but by abrupt, system-wide reconfiguration.

The Age of Transformation has begun. Capital must now act accordingly.

Navigating Systemic Risk in the Age of Planetary Phase Shift

The global financial system is facing escalating exposure to a category of risk it was never designed to model: the abrupt collapse of planetary stability. Emerging scientific evidence suggests that key components of the Earth system—particularly the Atlantic Meridional Overturning Circulation (AMOC) and the Southern Ocean overturning circulation—are destabilizing far faster than anticipated. These circulatory systems are foundational to global climate regulation, and their disruption could trigger irreversible, nonlinear transformations across physical and economic systems.

This report presents a scenario-based macro-financial risk assessment of such tipping points through 2050. It integrates the latest physical science with forward-looking economic modeling to evaluate the potential impacts of ocean circulation weakening or collapse. Our purpose is to provide institutional investors, asset owners, and financial system stewards with actionable foresight to navigate the implications of an increasingly unstable planetary operating environment.

We apply the Planetary Phase Shift Theory (Ahmed, 2024) as an analytical framework. It interprets the convergence of climate, ecological, and socio-economic disruption not as a series of isolated crises, but as symptoms of a deeper, nonlinear civilizational transition. In this framework, Earth system tipping points translate into tail risks for markets, institutions, and entire economies—posing challenges to solvency, insurability, and value preservation.

Why Now

Until recently, models projected that collapses of the AMOC or Southern Ocean overturning were possible only well beyond mid-century. That assumption is now under urgent revision:

- Recent observational and modelling breakthroughs (Li et al., 2023) show that the Southern Ocean overturning may decline by >40% by 2050, with critical freshening and stratification already underway.

- Statistical early-warning signals suggest that the AMOC may collapse as early as the 2040s under continued emissions (Ditlevsen & Ditlevsen, 2023).

These developments suggest that the Tail-risk scenario is no longer confined to distant futures—it may fall within the strategic horizon of current investment decisions.

Methodology & Analytical Framework

This report employs a three-tiered methodology:

- Tipping Point Identification

We synthesise the latest peer-reviewed science and physical climate models on ocean circulation weakening, meltwater dynamics, and feedback thresholds. - Scenario-Based Economic Stress Testing

We define three plausible 2050 scenarios—Central, Severe, and Tail—and estimate:- Global GDP deviation from baseline

- Sovereign credit risk (proxied through CDS spreads)

- Sector-level shocks (agriculture, infrastructure, insurance)

- Asset-Class Risk Translation

We map macroeconomic shocks to potential disruptions across global equities, sovereign bonds, real assets, commodities, insurance, and portfolio construction logic.

Structure of This Report

- Tipping Risk Primer: Scientific context for AMOC and Southern Ocean instability

- Macro-Financial Scenarios: Central, Severe, Tail – economic outcomes

- Asset-Class Implications: Transmission into equities, bonds, credit, real assets

- Strategic Scenario Architecture: 2050 economic trajectories under phase shift stress

- Investor Risk & Response Framework: Tools for resilience, adaptation, and strategic capital rotation

Earth System Tipping Points on the Brink

A Planet on the Edge of Nonlinear Change

Climate science increasingly points to the likelihood that key Earth system processes are approaching irreversible thresholds. These tipping points—where gradual change gives way to abrupt, self-perpetuating shifts—include critical components such as the Atlantic Meridional Overturning Circulation (AMOC) and the Southern Ocean overturning circulation. Both systems play a central role in regulating the global climate, redistributing heat and nutrients across the planet. Their destabilization would constitute not merely environmental disruption, but a global macro-financial shock with profound consequences for economic stability, investment portfolios, and global governance.

The Atlantic Meridional Overturning Circulation (AMOC)

The AMOC is currently at its weakest in over a millennium, having slowed by approximately 15% since the mid-20th century (Caesar et al., 2021). While the IPCC has deemed a full collapse this century “very unlikely,” emerging analyses challenge this view. A statistical study by Ditlevsen & Ditlevsen (2023) identifies rising variability and slowing recovery rates in key circulation metrics—classic early warning signs of a system approaching bifurcation. Their estimate places the potential for an irreversible collapse as early as mid-century under current high-emission trajectories.

If realized, an AMOC collapse would not just alter regional climates—it would trigger a nonlinear climate regime shift, reshaping temperature, precipitation, and storm patterns across the North Atlantic, Europe, West Africa, and the Americas.

Southern Ocean Destabilization: Antarctica's Failing "Lung"

At the other pole, a similar destabilization is underway. The Southern Ocean overturning circulation, responsible for forming Antarctic Bottom Water (AABW) and ventilating the deep ocean, is weakening rapidly. A high-resolution modelling study shows that AABW formation could decline by more than 40% by 2050 under unabated emissions (Li et al., 2023), driven primarily by meltwater from Antarctic ice sheets. This fresher, lighter water caps the denser saline water, preventing it from sinking and disrupting the deep ocean’s convective engine.

As one oceanographer put it: “If the oceans had lungs, [this overturning] would be one of them”—and its failure would have “huge impacts on lots of things” (England et al., 2023). These impacts include:

- Accelerated collapse of Antarctic ice shelves as warm deep water intrudes

- Nutrient stagnation in the abyssal ocean, starving surface productivity

- Disruption of global heat and carbon uptake, compounding climate feedbacks

Cascading Tipping Points: The Risk of Systemic Amplification

Importantly, these systems do not exist in isolation. Ice sheets, permafrost regions, tropical forests, and monsoonal systems are also exhibiting signs of increasing instability (Lenton et al., 2019). This raises the probability of cascading tipping points, where the collapse of one system (e.g. AMOC) increases the likelihood of tipping others (e.g. Greenland Ice Sheet, Amazon rainforest).

Steffen et al. (2018) warn of a potential transition to a "Hothouse Earth" scenario—where feedback loops involving ocean circulation, ice sheet collapse, and biosphere degradation push the Earth into a permanently hotter, less habitable state. In this scenario, global warming exceeds 4–5°C, sea levels rise by tens of meters, and the window for human adaptation rapidly closes.

From Climate Risk to Systemic Financial Risk

The convergence of these destabilizing signals is not merely an environmental issue. It constitutes a civilizational-scale risk event. The probability of non-linear disruption—where small changes abruptly shift the global climate system into a new regime—translates directly into tail risk for the global economy. Financial markets, built on assumptions of historical continuity, are poorly equipped to model such phase shifts.

In short: these are not just climate risks. They are macroeconomic shock risks. For long-term institutional investors, they represent a new category of systemic exposure: the threat that the planetary operating environment itself may transition into a state where current business models, valuation frameworks, and credit assumptions no longer hold.

Scenario-Based Macro-Financial Impacts

From Physical Tipping to Financial Tail Risk

The macroeconomic consequences of Earth system tipping points extend far beyond the bounds of gradual warming. While most climate-economy models assume linear, incremental damages, the activation of climate tipping points introduces a new regime of risk: discontinuous, self-reinforcing shocks to economic output, creditworthiness, food systems, and infrastructure. These dynamics are poorly captured by traditional macro-financial models that extrapolate from historical data. Yet for forward-looking investors, such non-linear risks increasingly define the contours of the 21st-century financial landscape.

The Limits of Conventional Modelling

Even absent tipping points, climate stress tests suggest substantial macroeconomic losses. The Swiss Re Institute projects that under a high-emissions scenario (~3.2°C warming), global GDP could be 18% lower by 2050 than in a no-climate-impact baseline. Under moderate warming (2–2.6°C), GDP losses still range from 11–14% (Swiss Re Institute, 2021).

These forecasts, however, assume smooth adaptation to rising climate damages. Tipping point dynamics introduce a structural break—economic losses no longer accumulate linearly, but arrive as clustered, compounding shocks with the potential to overwhelm adaptive capacity.

Tipping Points and the Fat-Tailed Distribution of Loss

Dietz et al. (2021) integrate tipping elements into climate-economic models and find that:

- The expected social cost of carbon rises ~25% compared to linear models

- There is a 10% probability that tipping events could double economic damages

- A 5% probability exists for tripling damages

This significantly fattens the left tail of the global GDP loss distribution, creating a new class of low-probability, high-impact financial risks. In such scenarios, climate shocks undermine not only economic output but the basic operating assumptions of fiscal solvency, infrastructure functionality, and insurance system stability.

Illustrative Tipping Scenario: AMOC and Antarctic Disruption

Regional Climate Dislocation

A collapse of the AMOC would cause dramatic shifts in regional climates:

- Northern Europe could cool by several degrees, shortening growing seasons and increasing energy demand

- Tropical rainfall belts and monsoons could shift or weaken, causing drought in South Asia and West Africa and flooding in others

- North Atlantic storm tracks could become more volatile and persistent

These shifts are not hypothetical. Model projections and paleo-climatic analogues suggest that abrupt AMOC shutdowns have previously reorganized global climate within decades (Ditlevsen & Ditlevsen, 2023; Lenton et al., 2019).

Sectoral Disruption: Agriculture and Food Security

- An AMOC collapse could cut UK agricultural productivity by up to 50% (Peterson, 2024).

- Rain-fed agriculture in Africa and Asia could suffer large-scale crop failures.

- The collapse of Southern Ocean overturning would reduce nutrient upwelling, potentially disrupting 75% of global phytoplankton production, threatening marine food chains and fisheries (England et al., 2023).

The resulting food price spikes, commodity volatility, and protein supply disruptions would cascade through supply chains, hitting both producers and consumers and amplifying risks of civil unrest and migration.

Tipping Points and Sovereign Risk Repricing

Sovereign credit is particularly sensitive to climate instability. Even under non-catastrophic scenarios:

- Cambridge researchers estimate 63 sovereigns could face credit rating downgrades by 2030 due to climate exposure, averaging ~1 notch (Klusak et al., 2021)

- In a high-emissions world, by 2100, ~80 countries could suffer multi-notch downgrades (some up to 6 notches)

These estimates exclude abrupt tipping events. In shock scenarios, sovereigns facing acute physical or food-system disruptions could face sudden CDS spread blowouts, capital flight, and rating “cliff effects.”

Examples include:

- Cooling-induced crop failures in Europe or energy crises causing fiscal strain in advanced economies

- Inundation or salinization of small island and delta nations, rendering portions of their land economically nonviable

- Climate-migratory pressure overwhelming public services, triggering political instability and loss of investor confidence

Empirical evidence already links climate vulnerability to higher sovereign CDS spreads (Naifar, 2023). Tipping points would amplify this differentiation, driving a wedge between climate-resilient “havens” and vulnerable sovereigns trapped in climate–debt feedback loops.

Multi-Sectoral Impact Matrix

The broader economic fallout from tipping-induced shocks would ripple through multiple sectors:

|

Sector |

Impact

Mechanism |

Likely

Outcomes |

|

Agriculture |

Precipitation shifts,

temperature extremes, ecosystem loss |

Crop failures, food inflation,

trade disruption |

|

Insurance |

Correlated disasters overwhelm

models and capital |

Withdrawal from high-risk

areas, uninsurability, insolvency risks |

|

Infrastructure |

Sea-level rise, extreme

heat/cold, storm damage |

Write-downs, capex spikes,

stranded assets |

|

Energy |

Hydropower loss, wind pattern

shifts, grid exposure |

Intermittency shocks, higher

costs, stranded generation assets |

|

Labor Productivity |

Extreme heat, disease vectors,

displacement |

Lower economic output,

especially in developing economies |

|

Credit Markets |

Sector and sovereign risk

repricing |

Widened credit spreads, rising

defaults, tighter financing |

This matrix illustrates how tipping events do not just produce sector-specific losses—they cascade across systems, undermining interdependencies that financial markets depend on for stability.

Systemic Shock, Not Linear Drag

Traditional models depict climate change as a drag on GDP growth. But tipping points signal a fundamentally different risk regime: one in which previously stable economic relationships break down, and markets are forced to reprice the value of capital, labor, land, and security in a volatile planetary environment.

Investors who fail to account for these non-linear dynamics are likely underestimating downside risk across portfolios. The next section maps these insights directly to asset class vulnerabilities and financial system stability.

Asset-Class Implications in a Phase-Shifted World

A Tipping Event Is Not a Sectoral Shock — It’s a System-Wide Repricing

Earth system tipping points—especially an AMOC or Southern Ocean collapse—would not remain confined to any one sector, country, or asset class. Their systemic nature ensures that such events would precipitate a simultaneous, cross-asset repricing, challenging the foundational assumptions underpinning modern portfolio theory. Volatility correlations would rise. Traditional hedges could fail. The result: a disorderly transition into a new financial regime marked by uncertainty, liquidity stress, and pervasive impairment of long-duration value.

Equities: The Collapse of Growth Assumptions

Global equity markets, rooted in expectations of future earnings and growth, are particularly exposed to the abrupt climate and macro disruptions associated with tipping points.

- Direct physical exposure: Firms in agriculture, fisheries, housing, and tourism face existential threats from asset damage, supply-chain shocks, and demand collapse.

- Indirect macro drag: Broader economic contraction and rising adaptation costs lower aggregate profitability across sectors, including tech, manufacturing, and consumer goods.

- Valuation compression: As risk premia rise and earnings become more uncertain, price-to-earnings multiples could contract sharply. Market consensus would shift from a growth-oriented paradigm to one of preservation and resilience.

For example, if the AMOC collapse drove a multi-year European agricultural failure and energy price spike, equity indices heavily weighted to Europe or emerging markets would likely underperform, while climate-resilient regions might benefit from capital rotation.

Emerging divergence: A premium would likely develop for firms with business models aligned to adaptation or decarbonisation (e.g. climate-smart agriculture, distributed energy, resilient infrastructure). Conversely, carbon-intensive or physically exposed companies would face devaluation or outright collapse.

Sovereign Bonds and Credit: From Risk-Free to Risk-Repriced

Sovereign bonds—often treated as the foundation of low-risk portfolios—would face mounting pressure:

- Rating downgrades: Countries exposed to chronic physical risk or acute disasters would suffer ratings pressure, increasing refinancing costs.

- Fiscal stress: Public balance sheets would strain under rising disaster recovery, adaptation infrastructure, and loss of tax base from economic disruption.

- Cliff-edge repricing: In a tipping point scenario, previously stable sovereigns could experience sudden credit risk repricing. Even advanced economies (e.g. UK, Germany) might see yield spreads widen if an AMOC-induced cooling hampers infrastructure and growth.

Emerging markets would be hit hardest:

- CDS spreads on climate-vulnerable sovereigns could spike.

- Default risk would rise as sovereigns contend with falling output and higher borrowing costs.

- Capital flight may trigger balance-of-payments crises in countries reliant on external financing.

Corporate credit markets would mirror these dynamics. In climate-exposed sectors, default probabilities rise as operating conditions deteriorate. Project finance would be scrutinised for long-term viability under altered geographies (e.g. drought-prone hydropower, inundated logistics hubs).

Insurance and Reinsurance: The Breaking Point

The insurance sector is both a frontline buffer and a potential amplifier of systemic risk in a climate tipping context.

- Correlated losses from climate-linked mega-events (e.g. simultaneous floods, crop failures, and wildfires) challenge the core actuarial premise of diversified, uncorrelated exposure.

- Capital buffer exhaustion becomes likely under scenarios of successive multi-region catastrophes. Some firms may face solvency risk; others withdraw from entire regions.

- Insurability collapse: As extreme event frequency grows, insurers raise premiums beyond affordability or abandon coverage altogether—leading to zones of uninsurability.

This creates knock-on effects:

- Mortgage issuance halts where property cannot be insured

- Commercial credit lines dry up for uninsurable assets

- Real estate markets freeze, further stressing financial institutions

Already, early signs are visible: U.S. insurers withdrawing from California wildfires and Florida flood zones; European reinsurers demanding higher risk buffers.

If tipping dynamics accelerate, this trend becomes global and systemic.

Real Assets: Physical Viability in Question

Real assets—real estate, infrastructure, and physical commodity assets—are highly exposed to irreversible environmental damage.

- Real estate: Coastal cities may see property values collapse as sea-level rise, storm surges, and insurance retreat render land uninhabitable.

- Infrastructure: Ports, airports, energy grids, and transportation networks require massive retrofitting. Without adaptation, they face stranded-asset risk and loss of utility.

- Agricultural land: Productivity shifts northward; formerly fertile zones may suffer desertification or excessive flooding. Asset revaluation follows climatically driven yield divergence.

In a phase-shifted world, real assets are no longer "real" stores of value without climate resilience built in.

Commodities and Currencies: Instability and Scarcity

Tipping points would likely generate supply shocks in:

- Agricultural commodities: Simultaneous crop failures, especially in staple crops (wheat, rice, maize), could trigger sharp price volatility and even rationing.

- Energy commodities: Transitional dynamics could amplify volatility—e.g. disrupted wind patterns, drought-affected hydro, and fossil fuel price swings amid chaotic transitions.

FX markets would respond to sovereign risk divergence:

- Climate-vulnerable currencies may depreciate as capital exits

- Climate-safe haven currencies (if they exist) could attract inflows, generating new FX asymmetries

- Commodity exporters could experience volatility based on perceived resource scarcity or climate resilience

Correlation Breakdown and Portfolio Construction Failure

Perhaps most destabilizing is the correlation shift across asset classes:

- The traditional negative correlation between equities and bonds—a pillar of modern portfolio diversification—may break down if sovereign risk rises alongside equity volatility.

- Safe haven assets (e.g. sovereign debt, real estate) may lose their buffering capacity

- Volatility clustering across assets could become the norm, as systemic stress translates into market-wide repricing

Asset allocation models based on historical covariance structures—Markowitz portfolios, Value-at-Risk systems, beta-driven strategies—would increasingly fail to protect downside in a nonlinear risk regime.

Investor Takeaway: Expect the Unexpected

The core message is clear: Earth system destabilization introduces deep structural uncertainty that invalidates core assumptions about diversification, hedging, and capital preservation. For institutional investors, this mandates a shift toward:

- Resilience-oriented allocation

- Stress-tested asset selection

- Geographic and physical climate risk overlays

- Dynamic response strategies aligned to planetary signals

The next section explores how this systemic logic extends to the very foundations of global civilization—and what that means for capital markets operating under conditions of ecological phase shift.

Planetary Phase Shift – Systemic Risk and Civilizational Challenge

Tipping Cascades as Civilizational Threat Multipliers

The risks outlined so far—macroeconomic losses, sovereign debt stress, sectoral collapse—are not isolated financial shocks. They are the early tremors of a broader systemic rupture: the destabilisation of the complex, interdependent global system that underpins modern civilisation.

Climate tipping points are not merely physical disruptions. They are non-linear risk events that transmit through every pillar of society—from food and water systems to critical infrastructure, energy markets, geopolitical stability, and financial order. When multiple subsystems (e.g., AMOC, polar ice sheets, tropical forests, permafrost, monsoons) approach their respective tipping points, the probability of cascading failures rises sharply (Steffen et al., 2018; Lenton et al., 2019).

This introduces a new logic of systemic risk: one critical tipping event increases the likelihood of others, triggering feedback loops that escalate both biophysical and socio-economic breakdown.

The Polycrisis is a Phase Transition

A growing body of interdisciplinary analysis is beginning to frame climate change not as a standalone risk, but as part of a broader polycrisis—a convergence of multiple, interlocking crises spanning environmental degradation, food insecurity, energy volatility, economic fragility, and political instability.

This view is encapsulated in the Planetary Phase Shift Theory (Ahmed, 2024), which argues that we are now crossing a threshold from a relatively stable planetary regime—the Holocene—to a destabilised Anthropocene marked by runaway feedback loops, declining systemic resilience, and the potential for abrupt global transitions.

From this perspective:

- The climate system is not changing linearly. It is approaching critical thresholds that will alter the Earth’s energy balance and resource distribution.

- The global economy, deeply entwined with physical infrastructure, supply chains, and ecological services, is similarly vulnerable to phase change.

- The risks are not additive. They are multiplicative and recursive—amplifying each other across domains.

The implication is that humanity is no longer managing discrete problems, but navigating a civilisational inflection point: either toward systemic collapse or transformational reconfiguration.

Financial Risk Becomes Systemic Civilisational Risk

For institutional investors, this context transforms climate risk into something more profound: a test of the viability of capital allocation itself under conditions of biospheric destabilisation.

As Steffen et al. (2018) note, feedback-driven transitions toward a “Hothouse Earth” state—characterised by 4–5°C of warming and multi-metre sea level rise—may become self-sustaining once certain tipping cascades are triggered, even if emissions cease. Economic and financial modelling frameworks are not designed to handle such discontinuities.

This requires a fundamental reframing of fiduciary responsibility. Climate risk is not a parameter to adjust in spreadsheets. It is a potentially existential disruption to the foundational assumptions of growth, valuation, insurance, and sovereign solvency.

Existential Threat Meets Strategic Opportunity

Importantly, this does not mean collapse is inevitable. As Lenton et al. (2019) argue, we are entering a “planetary emergency”—not to alarm, but to underscore the narrow window for action. If tipping cascades remain within pre-catastrophic bounds, an intentional transition toward a net-zero, nature-positive economy could restore stability and create a new growth regime.

The bifurcation now facing capital markets is not simply between “risk” and “no risk.” It is between:

- An unmanaged phase shift—chaotic, unpriced, and systemically destructive

- A deliberate transition—guided by foresight, policy, and strategic capital allocation

This is the “Age of Transformation.” The macro context for all long-term investing is now shaped by whether the planetary phase shift is navigated by design or by disaster.

Strategic Implications for Capital Markets

The deep uncertainty of tipping points calls for a redefinition of financial resilience. This includes:

- Rethinking risk modelling: Incorporate discontinuities, feedbacks, and structural breaks into scenario planning.

- Redesigning portfolios: Build in resilience to non-linear shocks, climate volatility, and infrastructure fragility.

- Reevaluating value: Focus on companies, assets, and regions that enhance adaptive capacity and reduce systemic stress.

- Engaging policymakers: Advocate for rules, investments, and incentives that increase the probability of a controlled transition.

From this systems lens, climate-aligned investing is not only a matter of ethics or ESG optics. It is a core pillar of fiduciary defence—a way to avoid being caught flat-footed as the biosphere enters a new operating regime.

The Investor’s Role in Civilisational Transition

Investors are not passive recipients of risk. With trillions under management, they help shape the outcome. In this context, the role of long-term capital is twofold:

- Safeguard portfolios against tipping-driven macro-financial disruption.

- Channel capital into solutions that increase planetary and civilisational resilience.

This is what the planetary phase shift framework calls civilisational renewal: using capital to accelerate the emergence of systems—technological, infrastructural, ecological—that are fit for purpose in a destabilised Earth system.

Scenario Architecture and Macroeconomic Impacts of AMOC–Southern Ocean Destabilisation to 2050

Stress-Testing the Global Economy

To quantify the economic fallout of climate tipping points, this section develops a structured three-scenario framework that models the potential weakening or collapse of two key Earth system components:

- The Atlantic Meridional Overturning Circulation (AMOC)

- The Southern Ocean overturning circulation

These scenarios represent plausible states of the world by 2050 and estimate associated impacts across:

- (a) Global GDP deviation from a no-shock baseline

- (b) Sovereign credit risk, proxied via CDS spread changes

- (c) Sector-level disruptions, focusing on agriculture, infrastructure, and insurance

Estimates are informed by macroeconomic models, Integrated Assessment Models (IAMs), and empirical literature. They are globally aggregated, with regional variations highlighted where relevant.

Scenario Overview

|

Scenario |

Temperature

Trajectory (°C) |

Ocean

Circulation Status |

GDP

Impact by 2050 |

Sovereign

CDS Risk |

Sectoral

Disruptions |

|

Central |

~2.0°C |

Moderate weakening of AMOC and

Southern Ocean |

~3–5% below baseline |

Mild spread widening |

Localised agricultural losses,

rising insurance claims, adaptation costs |

|

Severe |

~2.5–3.0°C |

Significant slowdown of both

circulations |

~10–15% below baseline |

50–200bps CDS spread increase;

downgrades in EM |

Breadbasket losses,

infrastructure stress, insurance retreat begins |

|

Tail |

3.0°C+ |

Collapse of AMOC and Southern

Ocean overturning |

>20–30% below baseline |

CDS spreads >1000bps in

vulnerable sovereigns; defaults likely |

Systemic food failure,

insurance collapse, real asset writedowns, sovereign credit crises |

Central Scenario: Gradual AMOC Weakening (Baseline-Like)

(a) GDP Impact vs. Baseline

- Global GDP ~3–5% lower than a no-tipping baseline by 2050, broadly consistent with standard climate damage estimates under ~2°C warming.

- Effects are incremental and geographically uneven:

- South Asia and Sub-Saharan Africa: greater economic drag due to monsoon disruption and heat exposure

- Europe/North Atlantic: may experience temporary cooling due to AMOC slowdown, partially offsetting warming impacts

- Historical modelling (Swiss Re Institute, 2021) supports a ~4% loss by 2050 under <2°C warming.

- Impacts compound modestly over time but remain within historical variation for many economies.

(b) Sovereign CDS Spread Impacts

- Mild spread widening for climate-vulnerable sovereigns.

- CDS spreads in emerging markets rise by tens of basis points on average due to heightened default risk perceptions.

- Empirical work (Mallucci, 2020) shows even moderate disasters elevate CDS spreads, especially in small island or agrarian states.

- No systemic sovereign crises, but early signals of climate-debt feedback loops emerge.

(c) Sector-Level Shocks

- Agriculture: Monsoon weakening reduces yields in India and West Africa. Output losses are significant but manageable through adaptation (e.g. irrigation, crop substitution).

- Infrastructure: Coastal and energy infrastructure faces sea-level rise and heat stress. Impacts remain localised but increasingly capital-intensive to maintain.

- Insurance: Annual insured climate losses double by 2050, driven by rising claims. Sector remains solvent but premiums rise, and some markets (e.g. flood zones) become unaffordable (GDV, 2024).

Summary:

The Central scenario reflects a continuation of current climate-economic trends. Macroeconomic costs are chronic but not catastrophic, concentrated in vulnerable geographies. Financial systems adapt incrementally.

Severe Scenario: Significant Overturning Slowdown (Tipping Elements Activated)

(a) GDP Impact vs. Baseline

- Global GDP ~10–15% lower than baseline by 2050.

- Includes both direct warming effects (~3°C) and non-linear shocks from circulation disruption.

- Swiss Re’s upper-bound scenario (~2.6°C warming) yields ~14% GDP loss; AMOC tipping could push well beyond this.

- GDP volatility increases as compound shocks emerge:

- Crop failures in key breadbaskets

- Disruption of seasonal climate norms

- Losses from infrastructure damage and productivity decline

(b) Sovereign CDS Spread Impacts

- Widespread spread widening, with increases of 50–200 bps for exposed sovereigns.

- Small island states, drought-prone agrarian economies, and low-lying nations experience multiple-notch downgrades and restricted access to capital.

- CDS markets begin pricing in climate-adjusted sovereign credit curves.

- Advanced economies (e.g. Southern Europe) also face moderate spread shifts if adaptation lags or disaster costs spike.

(c) Sector-Level Shocks

- Agriculture: Multiple breadbasket failures become common. OECD estimates a 50% contraction in wheat viability and steep declines in maize under AMOC disruption.

- Infrastructure: ~20% of global infrastructure sites face >50% value loss if no adaptation occurs (Jessop, 2025).

- Insurance: Annual catastrophe losses double every decade. Market begins to retreat from high-risk zones. Private coverage becomes patchy; public systems face fiscal stress (Trust, 2025).

Summary:

The Severe scenario represents climate regime change without full collapse. Macroeconomic damages are large and accelerating, sectoral resilience begins to erode, and capital markets enter a structurally riskier phase.

Tail Scenario: AMOC and Southern Ocean Collapse (Low-Probability, High-Impact)

(a) GDP Impact vs. Baseline

This scenario represents a worst-case convergence of climate tipping elements—long viewed as deeply unlikely by mid-century. However, recent developments suggest that the timeline for collapse may be far shorter than conventionally modelled. Observations and high-resolution modelling (Li et al., 2023) indicate that production of Antarctic Bottom Water could decline by over 40% by 2050, with the system already weakening rapidly due to accelerating freshwater input from Antarctic ice melt. This raises the possibility that the Southern Ocean overturning may reach a critical threshold for failure within decades—not centuries.

A simultaneous AMOC collapse, projected as possible by the 2040s under high-emissions trajectories (Ditlevsen & Ditlevsen, 2023), would compound this disruption. Together, these twin circulation collapses would result in systemic Earth system destabilization—disrupting global heat, carbon, and nutrient flows in ways that undermine planetary habitability and global economic coherence.

In this scenario:

- Global GDP losses exceed 20% by 2050, plausibly reaching 30–35% under compounding shock assumptions (Nordhaus, 2000)

- Europe experiences abrupt 5–8°C cooling, crippling agriculture and infrastructure

- Tropical zones face lethal heatwaves, prolonged drought, and water stress

- Global sea-level rise surges, as Antarctic ice sheet disintegration accelerates under weakened deep-ocean ventilation

Traditional macroeconomic models cease to function reliably. The true cost is likely underrepresented by GDP metrics alone, encompassing mass migration, conflict, mortality, and ecological system failure.

(b) Sovereign CDS Spread Impacts

- System-wide sovereign defaults emerge as adaptive capacity is overwhelmed

- Vulnerable economies (e.g., small island states, deltaic nations, climate-stressed emerging markets) see CDS spreads explode beyond 1000 bps, indicating imminent default

- Even G20 sovereigns face fiscal strain as disaster response, infrastructure loss, and humanitarian costs balloon

- A new class of “climate junk” sovereigns emerges

- Multilateral interventions expand: climate-linked debt relief, GDP-indexed bonds, and new supranational risk-sharing mechanisms become necessary to preserve global liquidity

(c) Sector-Level Shocks

- Agriculture: AMOC collapse devastates monsoons; Southern Ocean failure impairs global nutrient cycling. Multiple breadbasket failures occur in succession. Global famine risk escalates.

- Infrastructure: West Antarctic Ice Sheet destabilisation drives sea-level rise measured in tens of centimetres per decade, overwhelming adaptation planning. Coastal cities face economic abandonment. Inland flooding and storm losses become chronic and unrecoverable.

- Insurance: The sector enters structural insolvency. Private markets withdraw from nearly all natural hazard coverage. Public backstops face collapse under the scale of claims. Risk transfer ceases to function.

Summary

Once deemed a remote, end-of-century risk, the Tail scenario now demands serious attention due to accelerating trends in both the North Atlantic and Southern Ocean. Recent observational and modelling breakthroughs suggest that deep-ocean circulatory collapse could unfold within investor-relevant timeframes—by the 2040s to 2050s—with catastrophic economic and financial consequences.

This scenario is no longer speculative science fiction. It is a plausible upper-bound pathway that challenges the assumption of a manageable climate future and forces financial institutions to plan for system-wide macroeconomic destabilisation and civilisational risk.

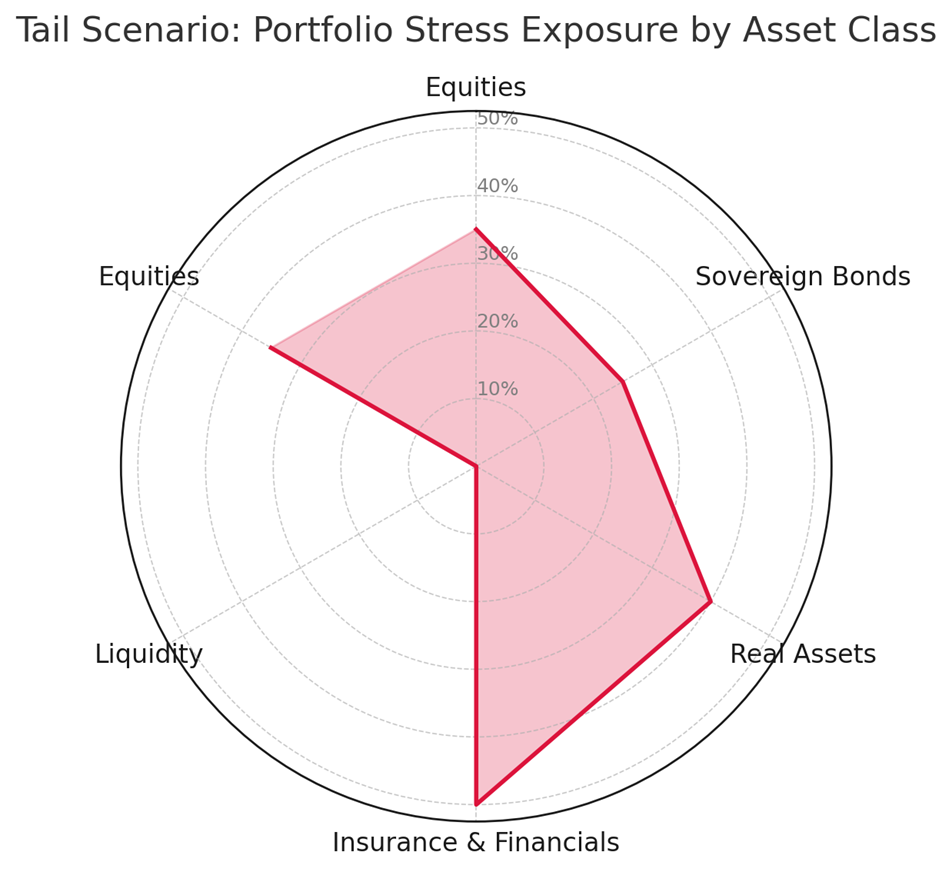

|

Asset

Class |

Allocation

(%) |

Tail

Scenario Impact |

|

Global Equities (including 15%

in EM) |

40% |

–35% due to systemic downturn,

food shocks, and sovereign instability |

|

Sovereign Bonds (incl. 10%

high-risk EM debt) |

30% |

–25%, with CDS spikes and

rating downgrades triggering repricing |

|

Real Assets (20% coastal RE, 5%

farmland) |

15% |

–40% coastal RE write-down;

farmland values diverge (North up, tropics down) |

|

Insurance & Financials |

10% |

–50% due to uninsurability and

reinsurance collapse |

|

Liquidity (short-term

sovereigns, gold) |

5% |

~0% (buffer preserved) |

Investor Response Strategy and Risk Management

From Risk Recognition to Strategic Response

The preceding analysis has established a sobering but actionable premise: the risk of a planetary phase shift driven by AMOC and Southern Ocean tipping events is no longer distant or abstract. The possibility that global oceanic circulation patterns could collapse within the next two decades places this threat firmly within the strategic horizon of long-term investors.

The challenge now is to shift from passive awareness to active risk management—while identifying opportunity spaces within the emergent climate-financial regime. This section outlines a comprehensive investor response framework designed to:

- Stress-test portfolios across all three scenarios (Central, Severe, Tail)

- Reallocate capital toward climate resilience, adaptation, and systemic mitigation

- Preserve long-term solvency and value under conditions of biophysical instability

|

Scenario |

Equities |

Sovereign

Bonds |

Real

Assets |

Insurance

/ Derivatives |

Cash /

Liquidity |

|

Central |

Overweight ESG-aligned tech and infra;

underweight fossil fuels |

Hold diversified sovereigns with moderate risk

buffers |

Moderate RE exposure in low-risk geographies |

Maintain CAT bond hedges and weather derivatives |

Maintain standard liquidity buffers |

|

Severe |

Underweight climate-exposed sectors; tilt to

adaptation-oriented equities |

Reduce duration in EM; overweight green

sovereigns |

Rebalance toward climate-resilient infrastructure |

Expand parametric insurance, long-dated hedges |

Increase liquidity to manage volatility |

|

Tail |

Minimal equity exposure; select climate-resilient

firms only |

Exit vulnerable sovereigns; shift to 'climate

haven' debt |

Focus on high-latitude farmland, off-grid assets,

water rights |

Avoid insurance exposure; systemic withdrawal

likely |

Prioritize maximum liquidity, short-duration

sovereigns |

1. Integrate Phase Shift Scenarios into Strategic Planning

Institutional investors must incorporate non-linear climate scenarios into strategic asset allocation (SAA), capital planning, and governance. This includes:

- Running stress tests across the Central (~4% GDP drag), Severe (~15% GDP loss), and Tail (>30% GDP collapse) pathways

- Modelling changes in:

- Value-at-Risk (VaR)

- Portfolio drawdowns

- Credit exposure by region and sector

- Expected return volatility

- Recognising that tail risks are now materially more likely due to recent ocean circulation findings

For example, if the probability of AMOC or Southern Ocean collapse rises from <1% to ~5–10% by 2050, traditional portfolio models must be recalibrated to reflect fatter tails. One study shows that including tipping point risks can increase expected long-term portfolio losses by over 10 percentage points (Waidelich et al., 2025).

2. Rebalance Asset Allocation Toward Resilience

Given the range of potential economic regimes, portfolios should be tilted toward systemic resilience and adaptive value:

Real Assets & Infrastructure

- Increase allocation to physical assets with low exposure to climate disruption (e.g. renewable energy, water rights, high-latitude farmland)

- Target resilient infrastructure with built-in flood/fire/storm protection

- Exit or hedge stranded real estate in low-lying, insurable regions

Equities

- Underweight climate-vulnerable sectors: conventional agriculture, fossil-fuel energy, insurance, low-resilience infrastructure

- Overweight climate-aligned growth sectors:

- Sustainable food systems (controlled environment agriculture, agritech)

- Climate analytics and early-warning systems

- Disaster-resilient construction and materials

- Energy decentralisation (microgrids, storage, smart systems)

- Prioritise firms with transparent, credible adaptation and mitigation roadmaps

Sovereign Debt and Credit

- Use climate vulnerability indices (e.g., ND-GAIN) and scenario-adjusted credit models

- Shorten duration exposure to high-risk sovereigns

- Consider climate-linked or GDP-indexed bonds in emerging markets

- Increase allocation to green sovereigns financing adaptation infrastructure

3. Employ Climate Hedging and Tail-Risk Protection

Markets increasingly offer tools to hedge phase shift-related shocks. These include:

- Catastrophe bonds: Event-triggered returns offset physical losses. Growing asset class as insurers transfer mega-cat risk.

- Weather and commodity derivatives: Useful for hedging agricultural exposure or heat/drought shocks.

- Long-dated index puts or tail-risk hedges: Protect equity portfolios against sudden devaluation in Severe or Tail scenarios.

- Parametric insurance: Indexed to climate thresholds (e.g. rainfall, temperature, storm intensity), offering faster, more predictable payouts.

Note: these instruments may fail to function in the most extreme conditions, so they should complement—not substitute—core asset reallocation.

4. Monitor Phase Shift Indicators and Early-Warning Metrics

Incorporate real-time climate science into financial risk dashboards. Key indicators to track include:

- AMOC strength metrics (e.g. RAPID array data, SST gradients)

- Southern Ocean overturning proxies (e.g. freshwater fluxes, stratification indices)

- Antarctic ice melt acceleration

- Deep ocean oxygenation and carbon uptake rates

Financial indicators to watch for tipping-point repricing:

- Rising CDS spreads for climate-vulnerable sovereigns

- Insurance premium surges or coverage withdrawal patterns

- Sectoral P/E de-ratings for exposed firms (agriculture, coastal RE, insurers)

- Volatility indices (VIX, commodity VIX) drifting above historical baselines

A cross-disciplinary signal dashboard should be treated as a planetary intelligence system—just as central banks use inflation forecasts or PMIs. Here is a sample monitoring dashboard:

|

Indicator |

Warning

Threshold |

Action

Implication |

|

AMOC Strength (RAPID Array) |

Sustained decline >15% vs

2004 baseline |

Shift fixed income from EU to global

diversifiers |

|

Southern Ocean Surface Salinity |

Net surface salinity rise

>0.5 PSU since 2015 |

Watch for feedbacks into heat

& CO₂ release |

|

Antarctic Sea Ice Extent |

Below 14 million km² at winter

peak |

Reassess Antarctic-linked real

asset exposure |

|

CDS Spreads on Climate-Exposed

Sovereigns |

Sovereign CDS >500bps or

multi-notch downgrades |

Hedge sovereign debt; reduce

exposure |

|

Crop Yield Volatility in

Breadbaskets |

Year-on-year yield swing

>20% |

Adjust agri investments;

consider food futures hedge |

|

Insurance Premium/Withdrawal

Index |

10+ insurers exit high-risk

regions |

Exit insurance holdings;

rebalance to resilience |

5. Advocate for Systemic Risk Internalisation

Institutional investors have both the incentive and leverage to push for policy frameworks that reduce tipping risk and support orderly transition:

- Engage with regulators and central banks to integrate tipping risks into macroprudential policy (e.g. climate capital buffers, sovereign risk stress tests)

- Support carbon pricing, green public investment, and international adaptation finance

- Back disclosure mandates (e.g. ISSB, TCFD+) that integrate non-linear climate risk

This is not philanthropy—it is fiduciary strategy. As Thallinger (2025) noted, without proactive mitigation, large segments of the global economy may become uninsurable. Financial institutions must help shift the system to remain solvent.

6. Invest in Civilisational Renewal

Beyond defensive repositioning, there are transformational investment themes that not only preserve value under tipping risk, but also enable systemic adaptation:

- Decentralised infrastructure: Solar microgrids, distributed water systems, off-grid health & education

- Climate intelligence tech: Predictive models, spatial risk mapping, adaptation logistics

- Circular resource systems: Materials recovery, closed-loop manufacturing, regenerative agriculture

- Risk-sharing innovation: Cooperative finance, disaster pooling, municipal insurance alternatives

These opportunities lie at the convergence of resilience, justice, and survivability—themes that will define the post-2030 investment landscape.

7. Maintain Liquidity and Optionality

In a phase shift environment, liquidity is not optional—it is existential:

- Hold larger-than-normal buffers in short-duration sovereigns and highly liquid equities

- Maintain hedging capacity and dry powder for opportunistic repositioning after climate-triggered market dislocations

- Avoid excessive lock-in to long-duration, illiquid assets that assume stationarity

Optionality also means strategic flexibility—the willingness to rebalance quickly as scientific and macro signals evolve. If AMOC collapse risk crosses a probabilistic threshold (e.g. >30% by 2040), even “low-probability” portfolios may become dangerously misaligned.

8. From Contingency to Core Strategy

The weakening of the Southern Ocean and AMOC circulations is not just a planetary anomaly. It is an emerging macro-structural threat to the financial system.

In a world where non-linear climate tipping points may arrive within the 2040–2050 horizon, investors must stop treating systemic risk as an appendix to ESG—and begin treating it as a foundational feature of long-term value.

Phase shift risk is no longer hypothetical. It is now a core parameter of portfolio solvency.

Top 5 Investment Opportunity Themes under Planetary Phase Shift Risk

|

Theme |

Why It

Matters |

Example

Opportunities |

|

Adaptation Infrastructure |

Extreme weather, sea-level

rise, and infrastructure fragility require systemic retrofitting |

Flood-resilient urban design,

elevated transport networks, cooling-integrated buildings, off-grid

microgrids |

|

Controlled Environment

Agriculture (CEA) |

AMOC and monsoon disruption

threaten traditional food systems |

Vertical farms, hydroponics,

indoor protein production, climate-resilient seed IP |

|

Climate Intelligence & Risk

Analytics |

Investors need real-time data

to monitor planetary tipping points |

AI-powered satellite

monitoring, tipping point early-warning platforms, climate-adjusted risk

indices |

|

Nature-Based Carbon Removal

& Regeneration |

Climate stabilization will

require massive drawdown, not just emissions cuts |

Rewilding, regenerative

agriculture, mangrove restoration, afforestation backed by high-quality

carbon credits |

|

Geoengineering & Planetary

Governance Tech |

Emerging tail-risk governance

frameworks will need robust oversight tools |

Stratospheric aerosol

monitoring, solar radiation control analytics, multilateral monitoring

technologies |

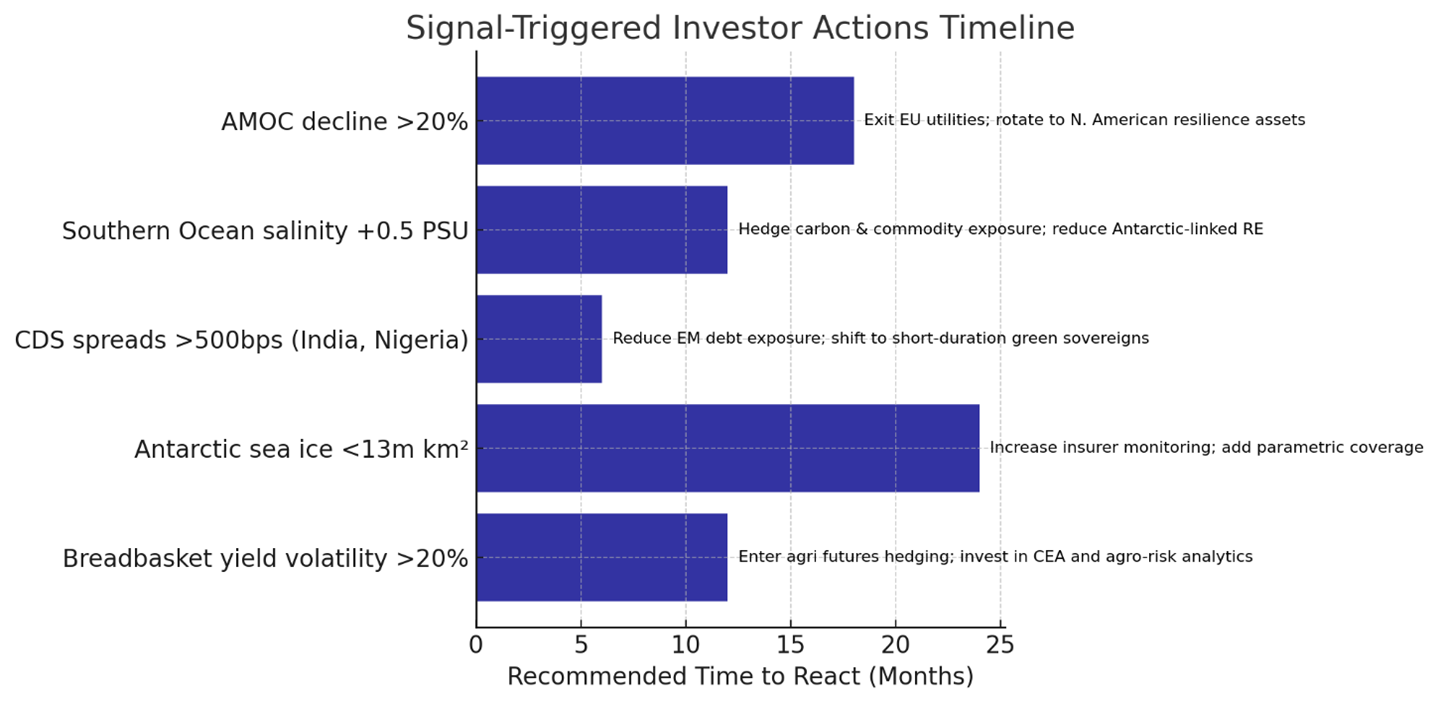

Signal-Triggered Investor Action Timeline

|

Signal

Detected |

Time

to React |

Investor

Action |

|

RAPID array shows >20%

decline in AMOC strength |

Within 12–18 months |

Exit EU utilities, tilt toward

North American resilience assets, increase CAT bond exposure |

|

Persistent rise in Southern

Ocean surface salinity (>0.5 PSU from 2015) |

Within 6–12 months |

Reassess Antarctic-exposed

holdings, hedge commodities with carbon futures |

|

CDS spreads widen >500bps on

India, Bangladesh, or Nigeria |

Within 3–6 months |

Reduce EM sovereign exposure,

rotate to short-duration green bonds in lower-risk markets |

|

Antarctic sea ice extent drops

below 13 million km² (record low) |

Within 1–2 years |

Increase monitoring of

sovereign and infrastructure insurers, add parametric coverage |

|

Wheat and maize yield

volatility exceeds 20% YoY in multiple regions |

Within 1 year |

Enter agri futures hedging

strategies, invest in CEA or agro-risk analytics |

Conclusion: Tipping Points, Capital, and the Planetary Crossroads

This report has presented an investor-grade analysis of one of the most consequential developments in modern human history: the destabilisation of Earth’s deep ocean circulation systems. Once deemed low-probability, long-horizon events, the weakening of the Atlantic Meridional Overturning Circulation (AMOC) and the Southern Ocean overturning circulation now show accelerating signs of nearing critical thresholds.

Recent advances in oceanographic modelling and observational data suggest that these twin systems—essential to regulating global temperature, precipitation, and nutrient flows—may undergo rapid collapse within the next two decades under current emissions trajectories. A full tipping event would upend physical climate systems and impose cascading macro-financial shocks beyond the adaptive capacity of markets.

The Investor’s Dilemma: Linear Tools in a Nonlinear World

Institutional investors today face a profound asymmetry. The tools that underpin portfolio construction—risk premia, volatility metrics, diversification models—were designed for a world of continuous, incremental change. But the planetary context is no longer incremental. It is transitioning toward nonlinear risk: discontinuous, compounding, and potentially irreversible.

This report has modelled three scenarios to 2050—Central, Severe, and Tail—each illustrating a deeper entanglement of ecological and economic systems. In the Central case, risks are severe but manageable through adaptation and policy reform. In the Severe case, financial resilience begins to erode. And in the Tail scenario—now within plausible reach—we confront the collapse of key planetary life-support systems, sovereign default contagion, insurance model breakdown, and capital market fragmentation.

The conclusion is clear: investors are no longer just exposed to climate risk—they are operating within a climate-restructured system.

Strategic Implications: From Risk Management to Planetary Navigation

The implication is not paralysis, but reorientation. Capital still matters. The financial system can either exacerbate planetary destabilisation by clinging to outdated assumptions—or it can become an engine for systemic resilience and transformation.

Investors must therefore:

- Price the unthinkable before it happens

- Reallocate capital to adaptive and regenerative systems

- Hedge exposure to deepening fragility across credit, equity, and real assets

- Engage with policy to internalise systemic risks and fund global adaptation

- Monitor Earth system signals as core indicators of financial regime change

This is not climate risk as usual. It is a civilisational inflection point. The decisions made by institutional capital over the coming years will influence not only financial outcomes—but the trajectory of the Earth system itself.

The Age of Transformation will be shaped by those who can see the difference between turbulence and rupture—between volatility that reverts to the mean and shifts that signal a new equilibrium entirely.

AMOC and Southern Ocean collapse represent more than extreme scenarios. They are markers of a rapidly closing window of planetary stability.

Investors who prepare for the phase shift—not just as a tail risk, but as a central strategic horizon—will be best positioned to survive it. Some may even help avert it.

Disclaimer

This report is published by Age of Transformation for informational and educational purposes only. It does not constitute investment advice, an offer or solicitation to buy or sell any financial instrument, or a recommendation to adopt any investment strategy. The views expressed are those of the authors and do not necessarily reflect the positions of any affiliated institutions, clients, or collaborators.

While reasonable care has been taken to ensure the accuracy of the information contained herein, Age of Transformation makes no representations or warranties as to the completeness, accuracy, or timeliness of the report or its contents. The information and projections provided are based on publicly available data, academic literature, and third-party sources believed to be reliable at the time of publication, but may be subject to revision without notice.

This report may contain forward-looking statements, including scenario analyses, estimates, and opinions regarding potential future outcomes. These statements involve inherent uncertainties and are not guarantees of future performance or events. Actual outcomes may differ materially from those expressed or implied.

Neither Age of Transformation, its authors, nor its affiliates accept any liability whatsoever for any direct or consequential loss arising from any use of this publication or its contents. Readers should seek independent financial, legal, and/or professional advice before making any investment decisions.

This publication is intended for a global audience, including institutional investors, policy professionals, the media, and the general public. It is not tailored to the specific investment objectives or financial circumstances of any individual or entity. Age of Transformation is not a registered investment adviser and assumes no fiduciary duty to any reader of this report.

{kind=link}